|

There was a soft patch during the previous global economic expansion. The Global Super Composite PMI--which we calculate by averaging the manufacturing and non-manufacturing PMIs for the US, UK, and EU--rose from a March 2003 recession low of 47.9 to a cyclical peak of 57.9 during January 2004. It then dropped back down to a 2005 low of 51.7 during May of that year before recovering to another cyclical peak of 57.1 during April 2006. It then hovered around 55 through August 2007 before starting a huge dive down to a record low of 37.6 during December 2008. What did stock prices do during the previous expansion’s soft patch? The S&P 500 rose during 2004 and early 2005, building on the bull market that had started in early 2003. So far during the current expansion, there was a brief soft patch last year in the Global Super Composite PMI, which declined from a peak of 56.7 during April to a low of 53.9 during September. The S&P 500 dropped 16.0% from April 23 through July 2. Concerns about a possible double dip were exacerbated by the sovereign debt crisis in the eurozone. But then the Super PMI rebounded to a new cyclical peak of 58.5 during February 2011. It then dropped to 53.2 during June. Meanwhile, stock prices have held up remarkably well following the rally from July 2 through April 23. We expect that the Super PMI will rebound during the second half of this year much the same as it did last year. If so, then stock prices should end the year higher than today. |

|

Auto sales are down sharply in recent months. There are two obvious explanations. The first is that the spike in the national average price of a gallon of gasoline to a peak of $3.96 depressed sales. The other is that a shortage of parts from Japan following the March 11 earthquake disrupted production and reduced the supply of models available for sale by auto dealers. Of course, it is likely that both explanations caused the drop in sales. The parts shortage should be over soon. The pump price is still high, but it was down to $3.56 during the week of June 29. At least, no one is talking about it rising to $5 a gallon. We expect a big rebound in auto sales during the last four months of the year. Total retail motor vehicle sales peaked during February at 13.4 million units (saar). They fell 14.9% to 11.4 million units during June. Over this same period, domestic light truck sales declined by 0.5 million to 5.0 million; domestic car sales dropped by 0.8 million to 3.9 million; and imported models fell by 0.7 million to 2.5 million. The decrease in imports was probably largely attributable to the plunge in exports of cars from Japan following the earthquake and tsunami. The decline in domestic car sales might have reflected both a shortage of parts and less interest in buying a car when gasoline prices were rising rapidly. Interestingly, sales of light trucks, which tend to be less fuel efficient, dropped the least, suggesting that parts shortages played a bigger role than higher gasoline prices in depressing sales in recent months. |

|

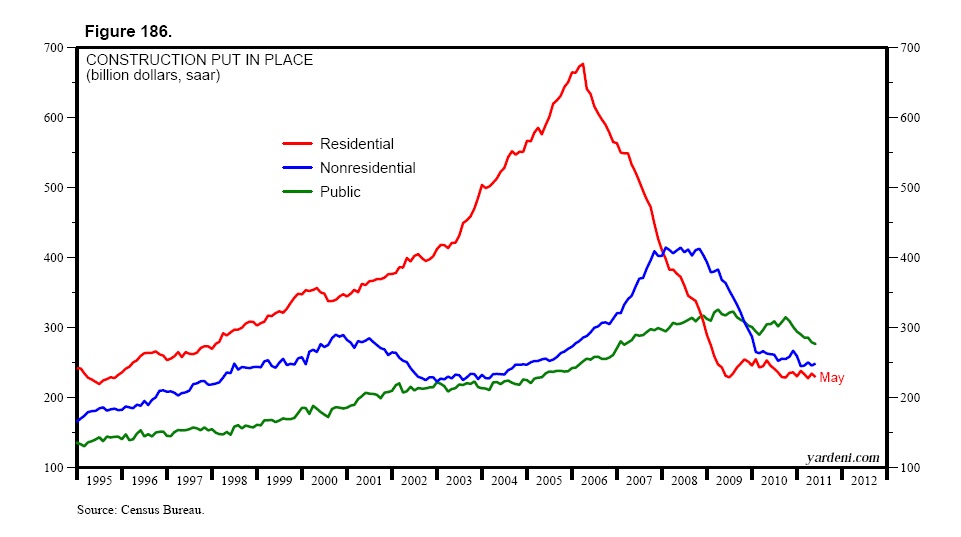

The rebound in the Super PMI should be led by a rebound in the global auto industry, including the one in the US. One US industry that is likely to remain stuck in the mud is construction. Indeed, the value of total construction put in place fell to a new recession low for the industry during May. It was $753.5 billion (saar), down 37.9% from the record high during March 2006 and the lowest since September1999. Here are a few more details on the sorry state of this industry: (1) The weakest sector in the industry remains residential construction. It peaked at a record $676.4 billion during March 2006. After crashing through 2008, it has been in a coma, flat-lining slightly south of $250 billion since late 2009. (2) Nonresidential construction has also been flat-lining slightly north of $250 billion since early 2010. Its hay days were during 2008, when spending was hovering around $400 billion. (3) Another clunker has been construction spending by the public sector. Despite all the money spent to stimulate the economy by Washington from 2009-2011, little of it stimulated public construction. Indeed, in May it was $276.3 billion, the lowest since February 2007 and actually down from a record high of $325.5 billion during March 2009. |

No comments:

Post a Comment